Contributed by: MatthewD, FreeTaxUSA Agent, Tax Pro

When you inherit stocks, property or other investments, you may have a capital gain to report on your tax return when you sell them. Using the tax provision known as the "step-up in basis" can reduce or eliminate the capital gains tax you owe.

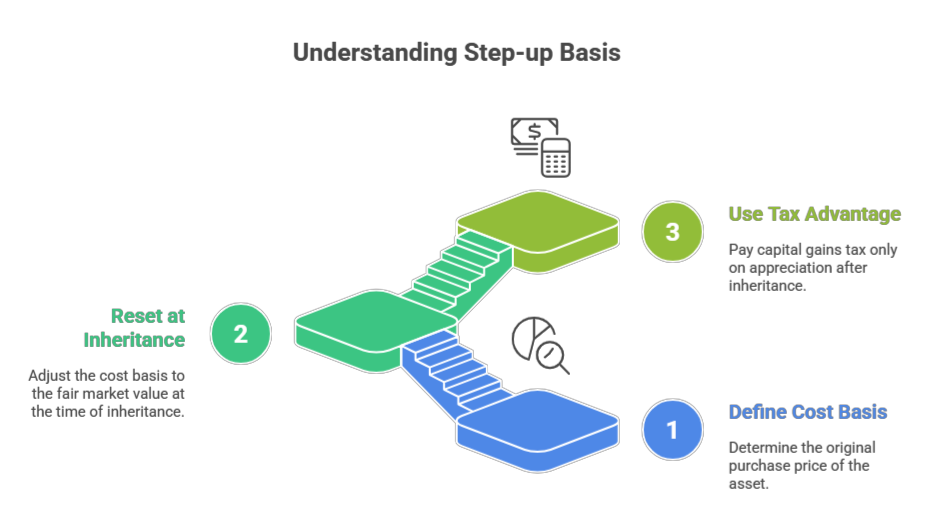

How step-up basis works:

- Defining cost basis: The first thing you need to determine is the cost basis of the inheritance. The cost basis is the original purchase price.

- Resetting the basis at inheritance: When you inherit something, the IRS "steps up" the cost basis to the fair market value (FMV) on the date of the original owner's death.

- Using a tax advantage: When you sell the inherited asset, you'll pay capital gains tax on the appreciation (increase in value) that occurred after the date of inheritance (i.e., after the basis was stepped up), not on the appreciation that happened during the original owner’s lifetime.

Spouse versus non-spouse inheritance

Whether you get an inheritance from a deceased spouse or someone other than a spouse, the tax treatment may vary. A surviving spouse or an heir will both benefit from a step-up in basis. However, for a surviving spouse living in a community property state, the step-up basis is applied differently than if you live in a separate property state.

Spouse inheritance:

- Community property state: In community property states (e.g., Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), both halves of community-owned assets typically receive a full step-up in basis upon the death of one spouse.

- Separate property state: In separate property states, only the deceased spouse's share of jointly held assets may get this basis adjustment.

- Valuation date: To take advantage of the step-up basis, use the fair market value on the date of death of the spouse.

Non-spouse inheritance:

- Valuation date: Step-up value in basis occurs on the date of death of the decedent.

💡 Note: In more rare situations, an alternate valuation date may be elected by the personal representative on an estate tax return. If that happens, the step-up value usually becomes either the fair market value of property six months after the date of death or the fair market value of the property on the date of distribution, sale, or exchange of the asset. The alternate valuation is only an option if it results in a decrease in the overall estate value and the estate tax liability.

Example of a non-spouse inheritance

Imagine your uncle bought a stock for $1,000, and it was worth $5,000 at his death.

If he had given you the stock as a gift while he was still alive, your cost basis would be the original $1,000. However, because you inherited it, your cost basis is stepped up to $5,000.

You sell it after a couple of years for $5,500. By utilizing the strategy, you'll only pay capital gains tax on the $500 gain ($5,500 - $5,000), rather than on the $4,500 gain ($5,500 - $1,000) you would have if you had been given it as a gift before your uncle’s death.

Example of a spouse inheritance

Community Property: If a couple in a community property state buy a house for $400,000 and the fair market value is $550,000 when the first spouse dies, then the surviving spouse’s new tax basis is $550,000.

Non-community Property: If a couple in a non-community property state buy a house for $400,000 and the fair market value is $600,000 when the first spouse dies, then only half of the $200,000 gain is added to surviving spouse’s tax basis, and the new tax basis is $500,000 ($400,000 + $100,000).

Things to consider

Asset Exceptions: Assets held in accounts like IRAs, 401(k)s, and most irrevocable trusts do not receive a step-up in basis.

Tax Savings: The stepped-up basis helps heirs and surviving spouses avoid or reduce paying capital gains tax on any increase in the asset's value during the original owner's life.

Estate Planning: The step-up rule is an important consideration in estate planning as it can help minimize the tax burden on your beneficiaries. Consider consulting with a tax professional or an estate attorney to assist you with your specific situation.

Alternate Valuation Date: Generally, it’s only used with estates valued over $13 million. The estate executor elects a valuation date six months after the descendent dies. However, the alternate valuation date applies only if the estate’s value decreases between the date of death and six months later, resulting in reduced estate taxes when filing Form 706. Typically, this is not a strategy used to reduce overall capital gains for the beneficiaries, since it reduces the step-up in basis.