Contributed by: PhillipB, FreeTaxUSA Agent, Tax Pro

Many people have rental properties that are co-owned with a group of people. Whether the group is your family or a pool of investors, knowing how to report rental income, expenses, and depreciation for co-owned property is crucial to filing a correct tax return.

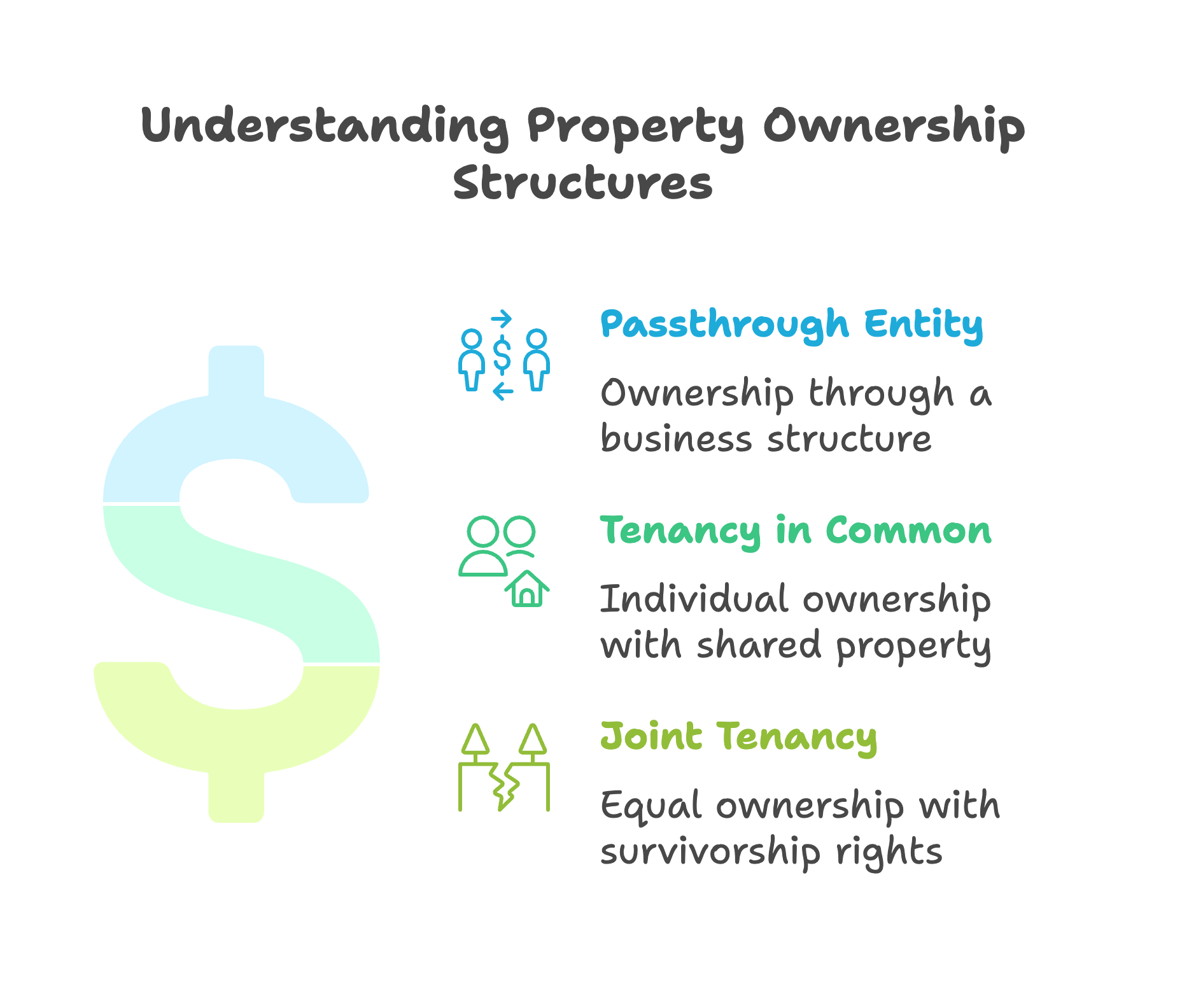

Different types of ownership

Rental properties may be held under various ownership structures. Some common forms of co-ownership are as follows:

- Owned in a passthrough entity, such as a partnership, S Corporation, estate or trust.

- Tenancy in common - two or more people each own a specific share of the property.

- Joint tenancy - two or more people own an equal share of a property together.

Ownership through a passthrough entity may be the simplest form of ownership to report the income for taxes. When a rental is owned through a passthrough entity, all net income or losses are reported on the passthrough entity’s informational income tax return, and each individual owner receives Schedule K-1 reporting their individual shares of the net rental income or losses.

If the property isn’t owned through a passthrough entity, each individual owner will be responsible for reporting their share of income, expenses, depreciation, and gains or losses.

Reporting co-owned income and expenses

Each owner will need to take the total income and expenses of the rental property and allocate these items to their ownership percentage.

For example, the Jones family owns and rents their deceased grandmother’s home. The property is owned by joint tenants with all four owners having a right to a quarter of the property. As a 25% owner of the property, Jeff Jones will allocate the following items of income and expense as shown below:

- Gross Rents – $30,000; 30,000 X .25 or 25% = $7,500 on Jeff’s return

- Property Taxes – $5,000; 5,000 X .25 = $1,250 on Jeff’s return

- Cleaning and Maintenance – $2,250; 2,250 X .25 = $563 on Jeff’s return

- and so forth for all expenses for the home....

Reporting depreciation on co-owned property

Each owner of a co-owned rental property will also be responsible for reporting their own depreciation on the property.

Continuing with the previous example, Jeff will enter the property as a depreciable asset in FreeTaxUSA by following these steps:

- Follow this menu path: Income > Business Income >Rental Income (Schedule E). Either select +Add a Rental or click edit next to a rental already in progress.

- On the Your Rental screen, click Depreciable Assets. Either click +Add an Asset or edit on the rental asset already started

- Enter all the main information on the screen labeled Tell us about your asset.

- If the property is rented full-time, the percentage of business use will be 100.0. If the property is used as a part-time rental, the business use percentage will usually be calculated by taking the number of days rented divided by the total number of days the home was used (days of rental use + days of personal use).

- For the Original Cost or Basis, Jeff will need to take the entire cost basis of grandma’s home and allocate his 25% ownership. If the home was inherited when grandma passed away in 2020, the inherited basis of the entire home would be the fair market value on the day she passed. For our example, we’ll use $300,000. Jeff’s original cost or basis would be $75,000 ($300,000 X .25 = $75,000).

- There’s one other asset screen that may require a calculation. On the screen labeled Additional Depreciable Asset Info, Jeff will be asked about the cost of land. If the home was appraised when his grandmother passed away, the appraisal should include a fair market value for the lot the home is on. If this is the case, using the appraised land value would be his Cost of Land (taking his 25% value only). If not, Jeff may need to make an educated estimate on the fair market value of the land on the date of his grandma’s death using any estimation method that’s reasonable and can be documented.

Key takeaways

The simplest form of rental property co-ownership may be through a passthrough entity. Having all gross income and expenses reported on one return eliminates the need for the individual owners to calculate their own shares separately. However, there’s a cost associated with having the annual informational return correctly prepared, so each owner has their Schedule K-1.

From a cost standpoint, owning rental properties in joint tenancy or as tenants in common may be more economical. If this is the case, every owner will need to make sure they have all the income, expense, and asset information to accurately calculate and report their share on their individual tax return.