Contributed by: Henry, FreeTaxUSA Agent, Tax Pro

With the recent signing into law of the One Big Beautiful Bill Act (OBBBA), millions of older Americans got a significant tax break through a new deduction available from 2025 to 2028. You may be wondering how the deduction works and if it affects social security benefits. Let’s look at the details so you know what to expect when tax time comes.

How much is it?

The maximum deduction is $6,000 per eligible taxpayer. For married couples filing jointly, the maximum deduction is $12,000 if both people qualify. No deduction is available if you’re married filing separately.

The deduction begins to phase out when modified adjusted gross income (MAGI) exceeds $75,000 ($150,000 for married filing jointly). It is reduced by 6% for every dollar over the threshold, phasing out completely at a MAGI of $175,000 ($250,000 if married filing jointly).

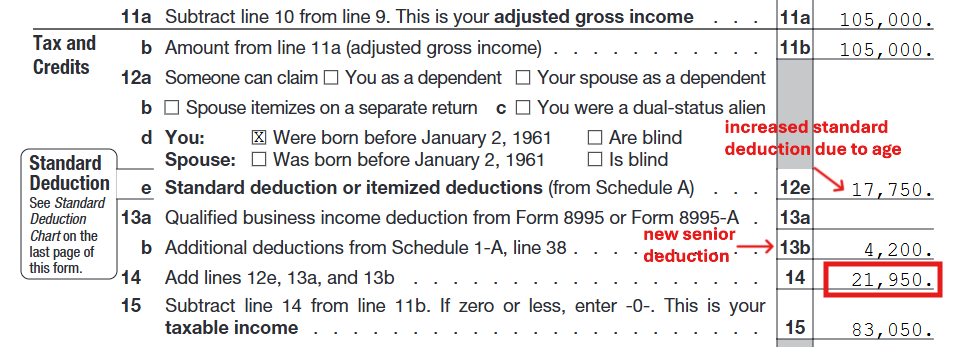

For example, Stephanie (age 67) is single and has a MAGI of $105,000. Since her MAGI is $30,000 over the threshold for her filing status, the deduction is reduced by $1,800 (6% of $30,000). Thus, her deduction is $4,200 ($6,000 - $1,800).

Who qualifies?

To be eligible for the new deduction, you must:

- Be at least 65 years old by the end of the year,

- Have a MAGI below the phase-out threshold for your filing status, AND

- Have an SSN valid for employment.

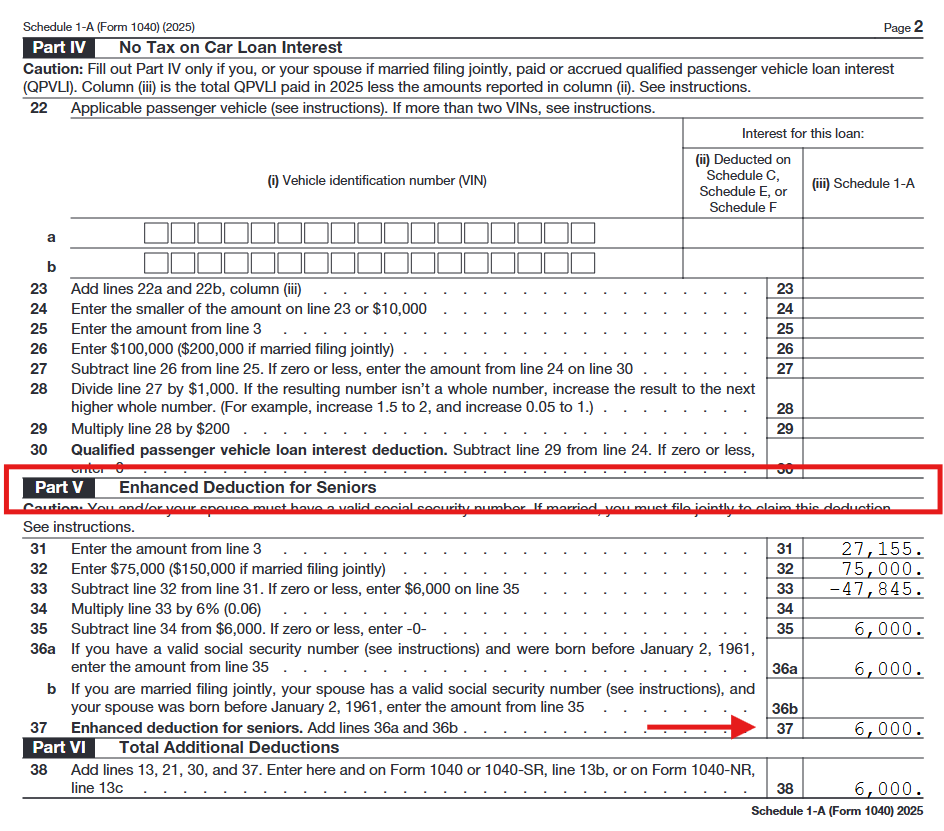

You can claim the new deduction regardless of whether you itemize your deductions or claim the standard deduction. The enhanced deduction for seniors is claimed separately on Schedule 1-A, a new tax form for 2025.

If you take the standard deduction, you’ll be happy to know the new deduction is in addition to the existing extra standard deduction for people age 65 and older or blind.

You’ll still use the standard deduction chart in the Form 1040 instructions or the chart on the last page of Form 1040-SR to figure your standard deduction and enter it on line 12e of Form 1040. Then the new senior deduction is applied on line 13b.

Going back to our earlier example, Stephanie’s 2025 tax return shows the regular standard deduction ($15,750) plus the $2,000 increase due to her age. Then she claims the new $4,200 deduction for a total deduction of $21,950 on line 14, as shown below:

Does it affect social security?

A recent message from the Social Security Administration caused some confusion among beneficiaries. The press release stated, “The new law includes a provision that eliminates federal income taxes on social security benefits for most beneficiaries, providing relief to individuals and couples.”

Many interpreted this as a new provision making social security benefits entirely nontaxable.

However, the next sentence clarifies this relief is achieved “by providing an enhanced deduction for taxpayers aged 65 and older.” In other words, it’s the $6,000 deduction that reduces taxable income, which in turn makes social security benefits nontaxable for many older taxpayers.

Under the OBBBA, social security benefits continue to be treated the same as under prior law, meaning they may be partially subject to income tax based on your total income for the year. The IRS formula requires you add your adjusted gross income, nontaxable interest, and half of your social security benefits. Then you apply the thresholds to see what percentage, if any, of your benefits are taxable. FreeTaxUSA software easily performs these calculations for you, and the taxable portion gets reported on line 6b of Form 1040.

The benefit from the new law appears further down on the form.

After calculating your adjusted gross income on line 11 of Form 1040 (which includes any taxable social security benefits), the standard deduction or itemized deductions are applied on line 12. For those who qualify, the additional $6,000 senior deduction is taken into account on line 13b.

Both deductions are then combined on line 14 and subtracted from adjusted gross income to determine taxable income. This means that even if some taxpayers have taxable social security benefits, the additional deduction will likely offset that amount for most seniors.

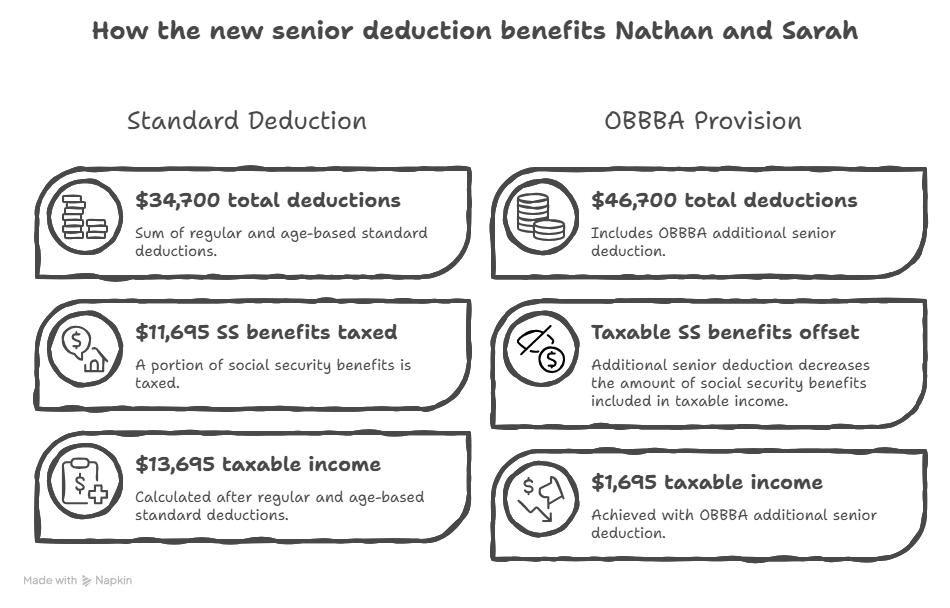

Let’s look at another example. Nathan, age 69, and his wife Sarah, age 67, both qualify for the additional senior deduction. They report the following on their 2025 tax return:

- $200 interest income

- $1,500 capital gains

- $35,000 taxable pension distribution

- $28,000 social security benefits, $11,695 of which are taxable

This gives them an adjusted gross income of $48,395. By applying the regular $31,500 married filing jointly standard deduction and the extra $3,200 standard deduction due to their age ($1,600 per qualifying spouse), they’re left with taxable income of $13,695 ($48,395 - $34,700).

However, when we add Nathan and Sarah’s additional deductions, their total deductions on line 14 of Form 1040 increase to $46,700 ($34,700 + $6,000 + $6,000). Thanks to the new OBBBA provision, they now have less taxable income ($48,395 - $46,700 = $1,695).

The additional $12,000 senior deduction offsets the $11,695 of taxable social security benefits, essentially making it so none of Nathan and Sarah’s benefits are taxed.

Conclusion

A significant change to tax deductions for senior citizens started with the 2025 tax return—potentially lowering your tax liability. When you’re ready to file your tax return, simply enter information about your age, filing status, and income into FreeTaxUSA software. We’ll handle the calculations to help ensure you receive the maximum deduction available for your situation.

Curious about other changes introduced by the OBBBA? Read this Community article, What are the top ten changes in the One Big Beautiful Bill Act? for a breakdown of the details.